Today is my baby brother’s birthday. He turns 17 and has been working part-time for a while now. I annoy him with unwanted advice about life, but I hope he soaks something in. Especially my talks about financial literacy, treating women with respect, and being responsible at parties.

In honour of his birthday, I will share some valuable knowledge about saving at a young age. In my opinion, saving when you’re young is way easier. Even though you don’t have a lot of money, you have far less expenses (if you have self-control). At 17/18 my only expenses were snacks, clothes, food if I ate out, and a bit of entertainment money. At 25, my expenses are all that plus cell phone, mortgage, internet, other bills, transportation, gifts, wine, fine cheese, travel, furniture, home decor, home maintenance and the list goes on and on.

Saving early also helps people develop good spending and saving habits. That way, as income increases, it won’t be a radical change to adjust savings and your lifestyle.

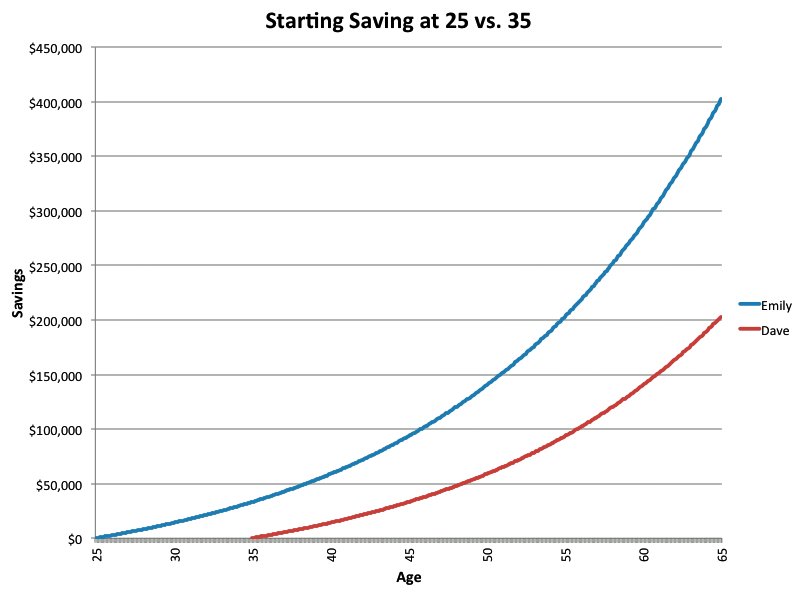

A powerful way to understand the importance of saving early is through a graph.

This information below is from Business Insider.

Consider two hypothetical savers, Emily and Dave. Emily puts $200 per month into a retirement account with an estimated 6% rate of return starting at 25. Dave starts saving $200 per month at 35, just 10 years after Emily.

Both continue to add $200 each month until they retire at 65.

By the time they are 65, Emily has contributed $96,000, while Dave has contributed $72,000.

Here’s the trajectory of both of those accounts: